The Data Center Refrigerant Market is experiencing unprecedented growth, with projections indicating a market size of approximately USD 581.1 million in 2024, expected to reach USD 1,268.06 million by 2035. This rapid expansion reflects an increasing demand for cooling refrigerants data centers, driven by a global shift towards energy efficiency and sustainability. The increasing complexity of cooling systems in data centers necessitates innovative refrigerants that can effectively manage thermal loads while minimizing environmental impact. Regulatory pressures are prompting organizations to transition from traditional refrigerants to more sustainable options, with significant implications for market dynamics.

As we analyze the current landscape, it becomes clear that North America is leading the Data Center Refrigerant Market, reflecting robust investments in energy-efficient HVAC cooling solutions data centers. According to Market Research Future, this region accounts for a substantial share due to its established data center infrastructure. In contrast, the Asia-Pacific region is emerging as the fastest-growing segment, fueled by rapid data center construction and heightened demand for advanced cooling technologies. Major players like Honeywell (US), Daikin (JP), Carrier (US), and others are actively investing in research and development to stay competitive in this evolving market, positioning themselves at the forefront of innovation.

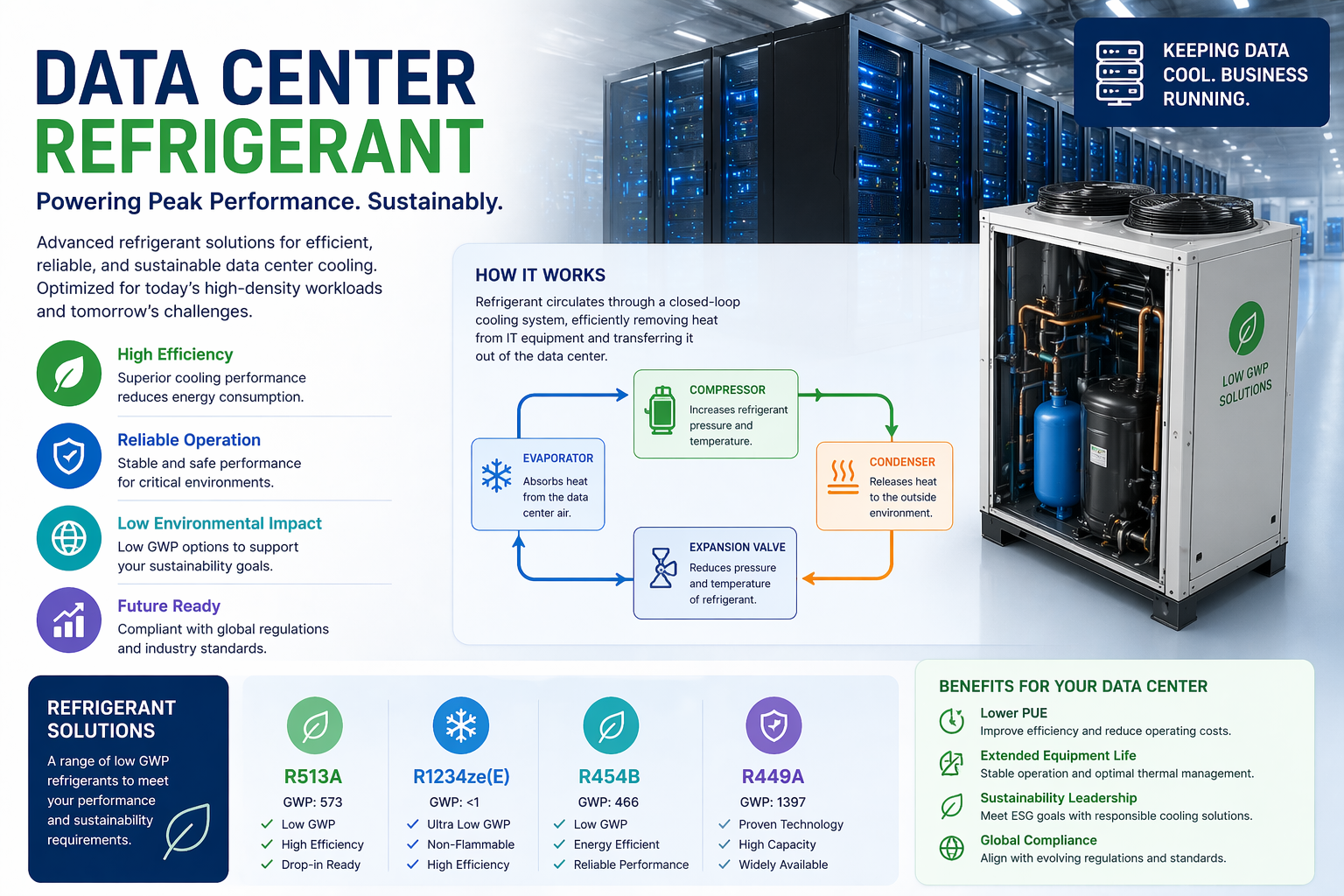

Several factors are driving the growth of the Data Center Refrigerant Market. Firstly, the push for sustainability is compelling organizations to adopt energy efficient refrigerants, which have a lower global warming potential (GWP). This shift is critical as companies aim to meet regulatory requirements and public expectations for environmental responsibility. Additionally, the increasing adoption of data center cooling technologies that utilize natural refrigerants is reshaping market dynamics, offering more environmentally friendly alternatives to hydrofluorocarbons (HFCs) which currently dominate the market. Companies like LG Electronics (KR) and Trane Technologies (IE) are leading initiatives to develop energy efficient cooling fluids, enabling data centers to operate at optimal conditions while reducing their carbon footprint.

In North America, the demand for HVAC refrigerants for data centers remains robust, with significant investments in infrastructure. The region's established data center market benefits from technological advancements in thermal management systems, ensuring high operational efficiency and sustainability. Conversely, the Asia-Pacific market is witnessing explosive growth due to rapid urbanization and the proliferation of digital technologies. Countries such as China and India are investing heavily in data center expansions, further driving the demand for efficient cooling solutions. This regional disparity in growth patterns highlights the need for tailored strategies to address specific market conditions The development of Data Center Refrigerant Market continues to influence strategic direction within the sector.

The Data Center Refrigerant Market is set to experience numerous opportunities as emerging trends, including the integration of AI in cooling systems and the increasing adoption of renewable energy sources, come to the forefront. Companies are now exploring innovative solutions to enhance cooling efficiency while minimizing energy consumption. Furthermore, as data center operators seek to optimize operations, the demand for data center cooling refrigerant systems will likely increase, providing a significant avenue for growth. With a projected CAGR of 9%, the market is poised to capitalize on these trends through strategic investments and partnerships.

The financial implications of this market growth are significant. For instance, according to the International Data Corporation (IDC), the global data center market is expected to reach USD 500 billion by 2023, necessitating a proportionate increase in cooling solutions. As data centers expand, the demand for more efficient cooling systems is expected to rise, with a projected increase of 25% in the adoption of low-GWP refrigerants by 2030. This trend is largely driven by stricter regulations on HFCs, which have a GWP up to 1,430 times that of carbon dioxide. A case in point is the European Union's F-Gas Regulation, which mandates a significant reduction in HFC usage, propelling the market toward natural refrigerants.

Looking towards 2035, the Data Center Refrigerant Market is expected to evolve significantly. Companies will likely focus on developing next-generation refrigerants that are both efficient and environmentally friendly. Innovations in energy management, alongside increased regulatory scrutiny regarding GWP levels, will shape the direction of the market. Experts anticipate that advancements in cooling technologies will lead to new applications and enhanced efficiency, enabling organizations to achieve their sustainability goals. These developments will not only transform the landscape of refrigerants but also create a competitive edge for market players.

AI Impact Analysis

Artificial intelligence (AI) is poised to revolutionize the Data Center Refrigerant Market by enhancing predictive analytics and real-time monitoring of thermal management systems. By leveraging machine learning algorithms, data centers can optimize energy consumption, reduce operational costs, and enhance the performance of energy efficient cooling fluids. Moreover, AI-driven analytics will enable more precise forecasting of cooling needs, ensuring that systems operate at peak efficiency while minimizing waste. This technological integration is not only beneficial for operational efficiency but also aligns with the sustainability goals increasingly prioritized by stakeholders.

Frequently Asked Questions

Access the report in Japanese, German, French, Korean, Chinese, and Spanish through our dedicated language pages

Marché des fluides frigorigènes pour centres de données